Lesson 022 - Practical Investing (TLDR)

Actionable Lesson With "Go-Do" Advice

My motivation and mission:

Google sheet that contains list of all WCD lessons and links to all content:

Lesson reviewing how to use Google sheet:

Too Long, Didn’t Read (TLDR). For anyone that follows reddit, they will know exactly what TLDR is. Effectively, it’s a reddit term for the summary of an article that hits all of the important points and usually has actionable steps that can be taken.

Lesson 022 is my version of a TLDR. It is a summary of simple and actionable steps that a new investor can take to getting on the path towards financial freedom.

Actionable Steps:

Adjust your life style to match you current income (need to save at least 10-20% of your income). You really should target 50%+ until you have reached financial freedom.

Paydown any bad debt (e.g. credit card debt that has an APR of 20%).

If your company has a 401K, max this out (there is a limit you can deposit per year).

Open a Fidelity* IRA and max this out with any remaining savings (there is a limit you can deposit per year). Invest in S&P500 or Nasdaq index funds.

Open a Fidelity* brokerage account and add additional savings into this. Invest in S&P500 or Nasdaq index funds.

Once you have enough saved for a down-payment, buy your first house. Make sure it is either a duplex/triplex/fourplex or has multiple bedrooms with their own bathroom. Start house hacking (L-15 - House Hacking).

As you continue to save more money, keep maxing out all of the tax exempt accounts (401k and IRA). Any additional savings can be added into your stock brokerage account or can be used as down payments on cash flowing rental properties.

*Fidelity is my preferred stock broker, but you can use any of the major stock brokers.

If I was to simplify the above steps it would be:

Adjust Life Style

Pay Down Bad Debt

Investment Priority 1 - 401k

Investment Priority 2 - IRA

Investment Priority 3 - Brokerage Account

Investment Priority 4 - House Hacking

Investment Priority 5 - Invest in Rental Properties

The steps above are a guideline/roadmap and are sequenced in an order that I believe to be the best. However, each individual is different and the stock market and real estate markets are dynamic, so there might be opportunities where it makes sense to change the sequence.

Below I will go into more detail about each of these steps.

Adjust Life Style

This step is the easiest and the hardest at the same time. Anyone has the ability to scale their life style down, but social pressures and ego keep many people trapped in their current spending habits.

Even engineers, doctors, and lawyers can get stuck in a trap where they are spending as much or more than they are earning. The number one key to your financial freedom is to SAVE and INVEST money.

This step takes a lot of humility.

The minimum you should target saving is 10% of your income. The higher this number is (especially in your 20’s and 30’s) the quicker your path to financial freedom.

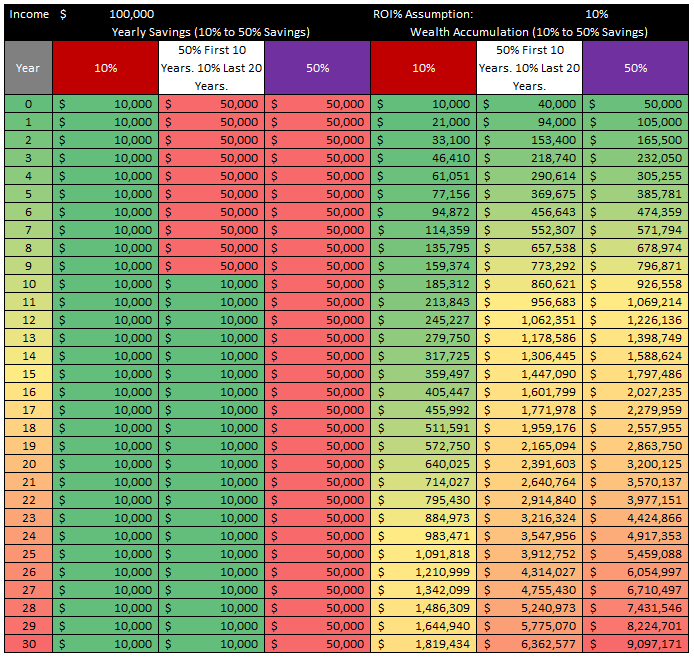

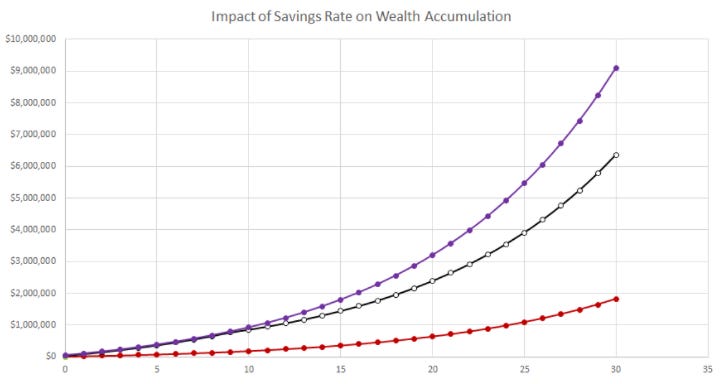

See example 1 below which capture the difference in wealth accumulation based on a 10%, 20%, 30%, 40%, and 50% savings rate. In all these cases, the individual is earning the same amount and getting the same ROI% on their investments. The only difference is the amount they are saving and investing each year.

10% - $1.82 million

20% - $3.64 million

30% - $5.46 million

40% - $7.28 million

50% - $9.10 million

You might notice that the amount of wealth you accumulate overtime is proportional to your savings rate. 50% savings accumulates 5x as much wealth as 10% savings.

Example 1 - Impact of 10% to 50% Savings Rate

I think a more powerful example is example 2 which highlights the importance of saving money early in your life. In example 2, there are still the same 10% and 50% cases as above, but now there is a middle case where the individual lives humbly for the first 10 years (saves 50% for these 10 years and then only 10% per year for all the remaining years).

Example 2 - Save Early in Life

10% - $1.82 million

Middle - $6.36 million (Save 50% first 10 years, then 10% for the remaining years)

50% - $9.10 million

This example definitely resembles my strategy in life. I lived very frugally in my 20’s and now I have a nest-egg that has grown substantially. Now I can justify a slightly higher life-style. The life style sacrifice in the first 10 years is the most impactful and it sets you up to enjoy the remaining years.

Pay Down Bad Debt

After you have adjusted your life style such that you are saving at least 10-20% of your income, the next step is to pay down all of your “bad” debt.

Bad debt examples

Credit card debt

Payday loans

Personal loans

Any “high interest” loan

Effectively, bad debt is any debt that is NOT used to acquire assets that earn you money and/or has a high interest rate.

Example 1

Let’s say you have $10,000 in credit card debt that has an interest rate of 20%. Do you pay off the debt or invest in the S&P 500? The S&P 500 provides an ROI% of roughly 10% per year.

$10,000 * -20% = -$2,000 (you will have to pay to credit card company)

$10,000 * 10% = $1,000 (you would have earned from investing in S&P)

The difference is -$1,000. Obviously, you would have been better off just paying off the credit card debt.

It’s actually quite simple. All you have to do is look at the interest rate. Effectively, the interest rate is a negative ROI. If the debt’s interest rate is greater than the expected ROI of an investment, you are better off paying down the debt.

Example 2

Let’s say you have $10,000 in credit card debt and it’s interest rate is 10% (the same as the expected ROI of the S&P 500).

In this case I would still paydown the debt. There is 100% certainty that you will have to pay the interest. There is a risk that the S&P does not provide 10%.

In any situation where the ROI’s between two investments are the same, you are generally better off taking the one with less uncertainty.

Investment Priority 1 - 401k

Once you have started saving at least 10%-20% of your income and have paid down all of your bad debt, now you can begin investing your money.

The first bucket you should put your money is a company’s 401K. This is a tax deferred account and typically the company will have a matching program. Effectively, the company will match your investment into the 401k up to a certain percentage.

I started my career at ExxonMobil making about $100,000 per year and they had a 7% 401k matching program. This means that I could deposit $7,000 into my 401k each year and ExxonMobil would deposit an additional $7,000. If I deposited $3,000, they would deposit $3,000. However, if I deposited $8,000, they would still only deposit $7,000 (that’s the 7% limit they would match).

Keep in mind that there is a yearly contribution limit to your 401K. This contribution limit is the maximum amount you can deposit in your 401k (not including the company match) that still gets tax benefits.

If you are fortunate enough as I was, you are able to save more money per year than the contribution limit.

There isn’t much point is contributing more than the limit, because the dollars you put in the 401k above this limit do not get the tax benefits.

Investment Priority 2 - IRA

If you are able to max our your yearly 401k contributions, then any spill-over savings can go into an IRA. The main benefit is that you don’t have to pay taxes on the capital gains in these accounts.

You can think of an IRA as effectively the same as a 401k, except you have greater control over the investments. Typically a company 401k will give you about 10 different investments that are available to you. A Fidelity IRA will give you access to effectively any publicly traded stock, mutual fund, or index.

There is also an IRA contribution limit. In 2021 this number was $6,000.

There is an additional restriction on Roth IRAs.

Effectively, in 2021, if you are filing as a single person, then you can’t contribute to a Roth IRA if your income is over $140,000 per year. (You can still contribute to your Traditional IRA).

…there is a way to backdoor money into a Roth IRA. This is a little loop hole that allows you to add money into a Traditional IRA and then roll it over to a Roth IRA.

Honestly, I don’t know if there is much benefit in doing this. I typically just deposit $6,000 into my traditional IRA each year. I could make an argument for why traditional IRAs are better than Roth IRAs.

I will create a dedicated lesson to discuss the differences between a Traditional and Roth IRA.

Investment Priority 3 - Brokerage Account

Consider the example below:

$100k income

25% taxes

25% of income used for life style and living expenses

Max out 401k ($19,500 in 2021)

Max out IRA ($6,000 in 2021)

This leaves $24,500 of additional savings for you to invest. Where do you put it?

This is a complex question that depends on the stock market, housing market, cryptocurrency market. This is where you, as an investor, have the freedom to do what you want. You could even use this money to start a business.

However, for most people, the next logical progression after a 401k and IRA is a brokerage account.

What is a brokerage account? This is just a regular (no-tax-benefits) account with a stock broker. At Fidelity it is labelled “INDIVIDUAL - TOD”.

Why is the next step for most people a stock brokerage account?

Because stocks are easy…

Investing in index funds is as passive as an investing gets. Most people don’t want to spend any time researching businesses, hustling, dealing with houses, etc. Therefore, for most people, if you have additional savings that you want to invest, open a stock brokerage account and start dollar cost averaging into index funds like the S&P500 and Nasdaq.

Investment Priority 4 - House Hacking

The reason I put house hacking as investment priority 4 is because it is something that not everyone will be willing to do. That being said, if you successfully house hack, then this can add more to your top and bottom line then any of the prior investments (401k, IRA, stock brokerage account).

What is House Hacking?

See L-15 - House Hacking. Effectively, house hacking is buying a property that you live in and rent out additional units or rooms that are associated with the property.

Examples:

Buy a 3 bedroom house, rent out the 2 spare bedrooms

Buy a duplex. Live in A unit and rent out B unit.

Buy a multifamily property. Live in one unit and rent out the remaining units.

Buy a single family home and build a separate apartment in the back yard that you rent.

Why House Hacking?

Housing is one of the largest expenses for any individual. House hacking can effectively eliminate this expense and potentially turn it into a profit.

There are also a lot of benefits from owning property which I outlined in L-10 - Real Estate & REITs.

House hacking is effectively just living with roommates that pay you. In many instances, the rental revenue you get can cover the mortgage.

My House Hacking Experience

I bought my home in 2016. I house hacked for 5 years. I was able to consistently rent out the two guest bedrooms for about $1,000 each giving me roughly $2,000/month or $24,000/year in rental revenue.

The numbers:

$371,000 purchase price. 3 bedrooms each with their own bathroom.

15% down payment >> $55,650

2.25%, 30 year mortgage. 5-year arm.

Loan amount = $315,350

Monthly mortgage = $2,300

Total monthly payment = $2650

*Total monthly expenses = $2,035

*The principal in the mortgage payment is your equity. This needs to be subtracted from monthly expenses… this is your money.

I’m going to glaze over the tax benefits because this gets complicated, but there are some major tax deductions for rental properties. You need to prorate these deductions based on the percent utilization (e.g. I was renting 2 out of 3 rooms in the house, so I would claim 66.6%).

You can see the image below for a summary of tax deductions. If I assume my tax rate is about 25%, then for every dollar of deductions I can remove from my AGI, then it saves me 25 cents of taxes that I would have to pay. This “tax benefit” can be thought of as a positive line item in your monthly expenses.

After you factor all of these things in, there is about a $600 positive cash flow. Some of this cash flow ends up in the equity of your house and some of this cashflow isn’t realized until you pay your taxes each year.

Therefore, I have turned what used to be a $1,500/month expense (renting an apartment) into a $600 benefit.

The difference between these two scenarios is $2,100 per month. This is roughly $25K each year! And this is post-taxes!

As a cherry on top, the house I purchased in 2016 has gained about $100k in value in the 5 years I have owned it.

My House Hacking Summary

Purchased $371,000 house with a $55,650 down payment.

My monthly cash flow (accounting for taxes and principal payments) went from -$1,500 per month to +$600 per month. $25k after-tax benefit for 5 years. $125k benefit to my bottom line.

My house gained $100k in value in 5 years.

Effectively, the $55,650 investment has turned into $225,000 in 5 years time. This is a 4x in 5 years. This is a 32% CAGR.

My benchmark for a good investment is 15%. I would say this was definitely one of the better investments I ever made.

Investment Priority 5 - Invest in Rental Properties

If you have:

Adjusted your life style to save a minimum of 10-20% each month

Paid off all your bad debt

Maxed out your 401k and IRA contributions

Bought a primary residence (hopefully house hacking it)

Then I think you are ready to start acquiring rental properties in your portfolio as diversification and a hedge against inflation.

The reason I left this one last is because it is the most amount of effort. I’m sure the people at BiggerPockets would advocate for you to focus on real-estate even before you have maxed out your 401k and IRA, but these accounts have tax benefits and are super easy to dollar cost average into.

Real estate takes an order of magnitude more work and the returns can definitely be lumpy.

Don’t let me talk you out of investing heavily into real estate; just keep in mind there is an opportunity cost to everything. The time and effort you spend in real-estate investing could be spent:

Developing additional valuable skills

Networking

Starting side hustles

With your family

I dive into real estate as an investment opportunity in L-10 - Real Estate & REITs.

Summary

Don’t like reading? Limited on time?

This lesson is a TLDR that summarizes actionable steps you can follow (with a suggested sequence) in order to get yourself on the path towards financial freedom.

Adjust Life Style (start saving at least 10-20%)

Pay Down Bad Debt (e.g. credit cards)

Investment Priority 1 - 401k (up to $19,500 per year)

Investment Priority 2 - IRA (up to $6,000 per year)

Investment Priority 3 - Brokerage Account

Investment Priority 4 - House Hacking

Investment Priority 5 - Invest in Rental Properties

Reference Material & Social Media

In Lesson 030 I cover how to navigate and utilize the Google Sheet I have built for all WCD lessons. This Google Sheet contains a worksheet for each WCD lesson. Each sheet has all of the Excel calculations, tables, graphs, and charts that I have posted in the respective WCD lesson. Additionally, the Google Sheet has a master “Index” worksheet that has links to all of the content associated with each lesson.

If you found this post helpful, please like, share, and follow me on my social media channels!